WHY APARTMENTS

Recovery Timeline for High-Supply Markets with Negative Rent Growth

Many of the high-supply development pipeline markets have created nearly a 20% increase in units in just three years. Ten of these 16 markets have reached peak deliveries while others peak in 2025. By mid-2025, multifamily construction starts are expected to be 74% below their 2021 peak and 30% below the pre-pandemic average. This change has begun to drive vacancy rates down, as exceptional renter demand continues from job creation, population growth and competitive discounting. These markets are expected to benefit from improved average vacancy rates and above average rent growth, while single-family housing market remains relatively unaffordable. Refinancing of commercial real estate remains a work in progress but does provide negotiating headroom in acquisitions.

Source: CBRE Research, Econometrics Advisors, Q3 2024, The Wall Street Journal

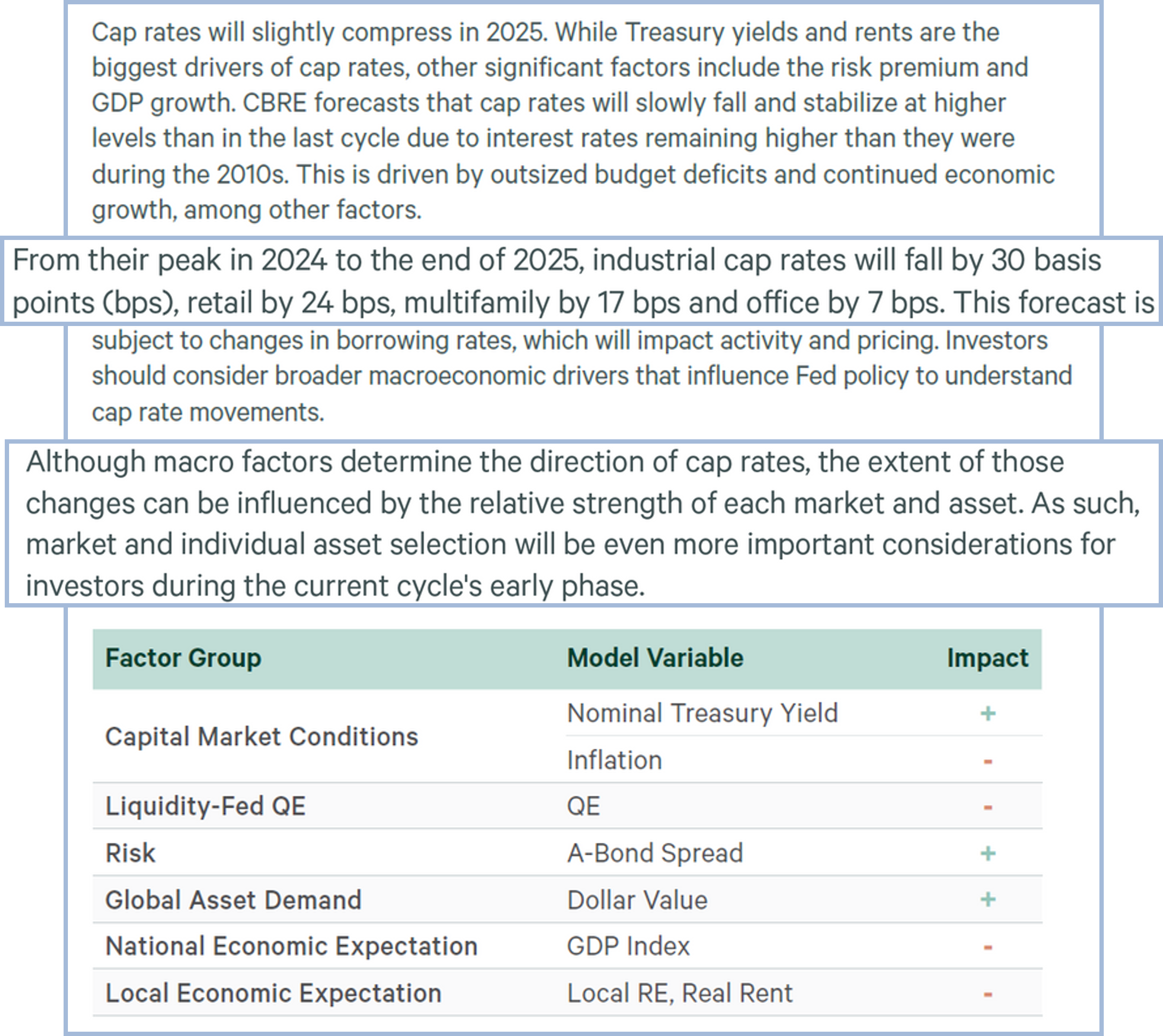

Current Outlook on Cap Rates

Source: CBRE Research, Econometrics Advisors, Q3 2024, The Wall Street Journal

Recovery Timeline for High-Supply Markets with Negative Rent Growth

Source: CBRE Research, Econometrics Advisors, Q3 2024, The Wall Street Journal

Many of the high-supply development pipeline markets have created nearly a 20% increase in units in just three years. Ten of these 16 markets have reached peak deliveries while others peak in 2025. By mid-2025, multifamily construction starts are expected to be 74% below their 2021 peak and 30% below the pre-pandemic average. This change has begun to drive vacancy rates down, as exceptional renter demand continues from job creation, population growth and competitive discounting. These markets are expected to benefit from improved average vacancy rates and above average rent growth, while single-family housing market remains relatively unaffordable. Refinancing of commercial real estate remains a work in progress but does provide negotiating headroom in acquisitions.

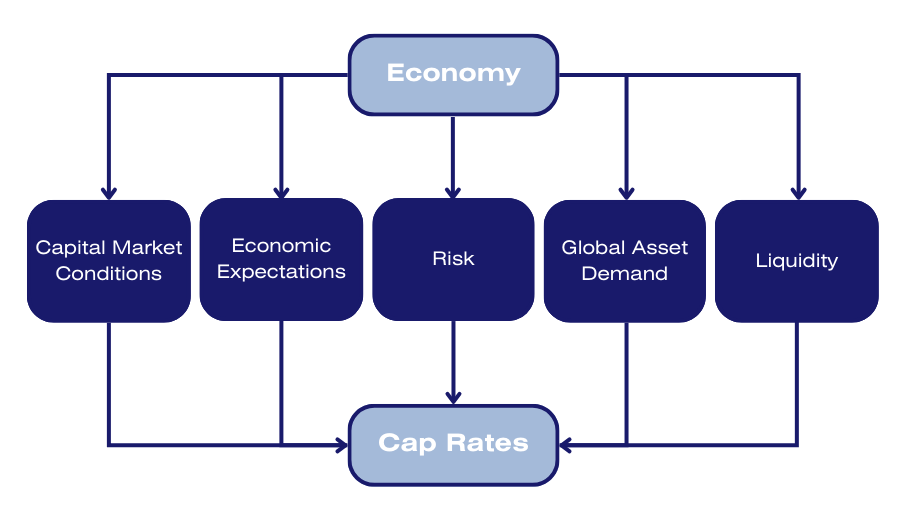

Current Outlook on Cap Rates

Source: CBRE Research, Econometrics Advisors, Q3 2024, The Wall Street Journal

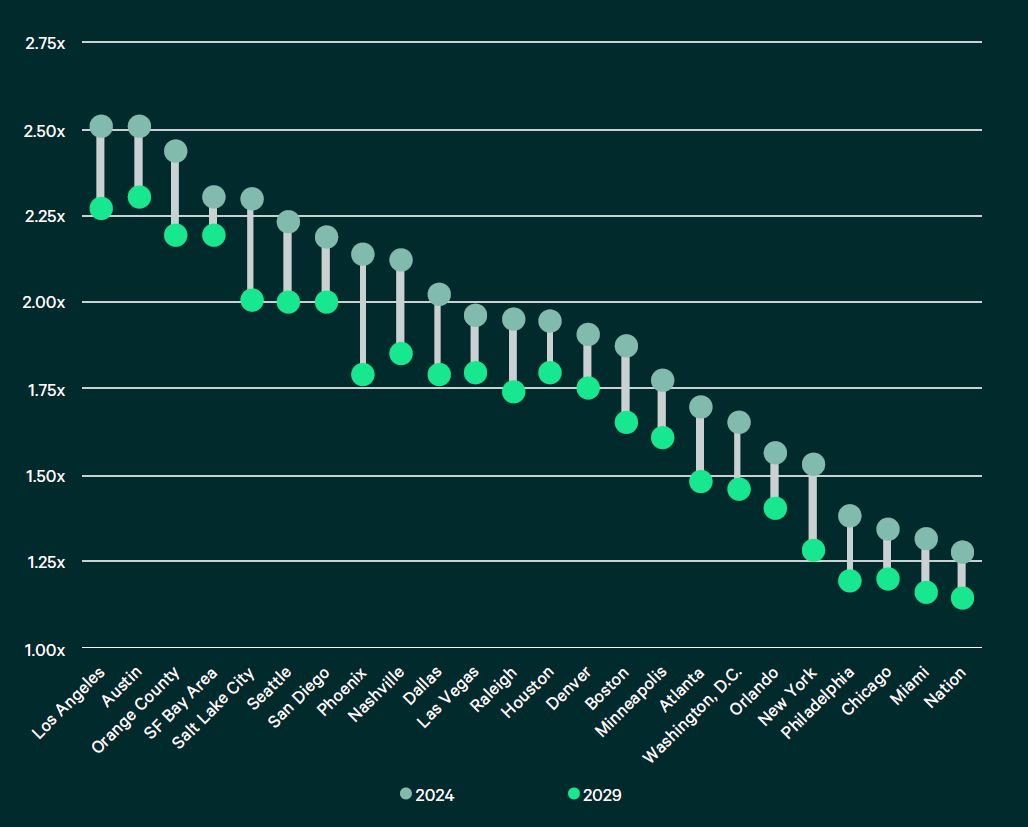

Cost-to-Buy Premium

"With average newly originated mortgage payments 35% higher than average apartment rents as of Q3 2024, many U.S. households continue to rent rather than buy a home. Even though the premium to buy a home is expected to down over the next several years based on home-price, interest-rate and rent-growth forecasts, it will remain high enough to keep today's renters renting for longer.

We expect average multifamily rents to grow by 3.1% annually over the next five years, above the pre-pandemic average of 2.7%. This above-trend rent growth is expected to outpace home price appreciation and, along with lower mortgage rates, slightly narrow the cost gap between buying and renting. CBRE expects the premium to buy versus rent to ease to 32% from 35% by the end of 2025.

All markets will see their cost-to-buy premium shrink over the next five years as interest rates fall, home price growth remains subdued and rent growth accelerates. Austin and Los Angeles have the highest cost-to-buy premiums in the country, both more than 2.5 times the average rent. Although that premium will come down over the next five years, it will remain more than twice as expensive to buy than to rent.

High-growth markets like Phoenix, Salt Lake City and Nashville will see the most premium compression over the next five years. This will be driven by above-average renter demand and reduced multifamily construction pipelines leading to accelerating rent growth."

Source: CBRE Research, CBRE Econometrics Advisors, Freddie Mac, Realtor.com, FHFA, Oxford Economics

Take Advantage Of Increased Tax Benefits

Our Team only acquires stabilized (above 80% occupancy) and cash flow positive apartment building investments. This allows our investors to make healthy returns while showing a loss at the end of every year.

Take advantage of 3 types of depreciation that allow investors to lower taxes:

1

Standard or Straight-line Depreciation

2

Accelerated Depreciation

3

Bonus Depreciation

Cost segregation studies are performed on all of our assets and the tax benefits pass through to our investors via annual year end reporting on K1s that are issued for the preceding year.

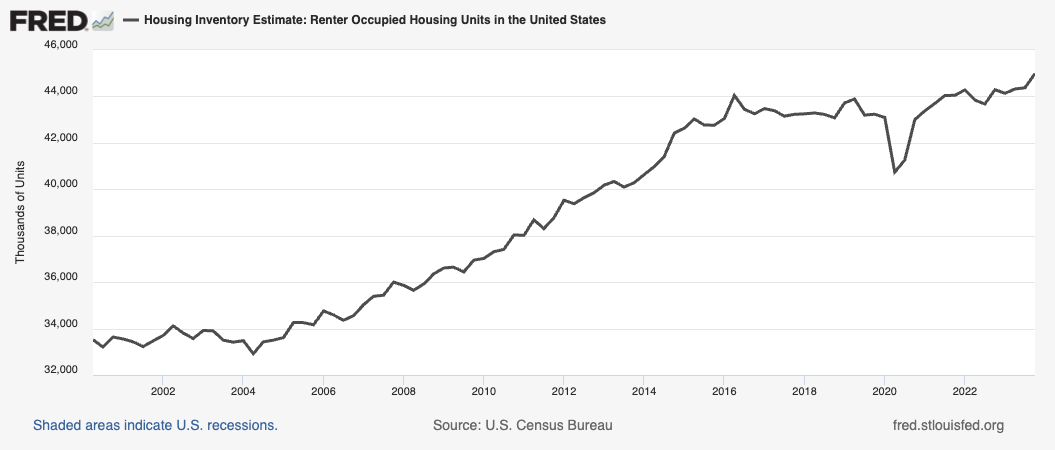

Demand for apartments is at an all-time high and still climbing

Since its peak in the mid-2000s, home ownership has been significantly dropping, and it will continue to drop as millennials, and aging baby boomers want to stay mobile in the 21st century.

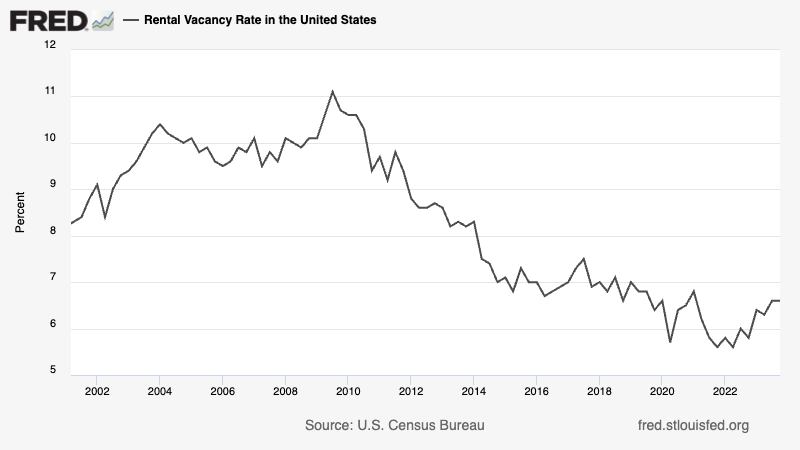

Vacancy rates remain low due to increased demand

With the population continuing to increase, demand for apartments is at an all-time high. This increase drives the need for apartment living higher and higher. Low vacancy rates equal more significant cashflow and equity growth, which translates to higher returns for our investors.

Investors Love Working With Us

Our focus is on building long-term, collaborative relationships with investors while handling the work needed to generate strong returns. Backed by extensive capital markets experience and relationships with institutional investors, we excel in driving transformational change and executing processes with expertise.

Contact us today to schedule a presentation and learn more—your success is our priority.

Investors Love Working With Us

Our focus is on building long-term, collaborative relationships with investors while handling the work needed to generate strong returns. Backed by extensive capital markets experience and relationships with institutional investors, we excel in driving transformational change and executing processes with expertise.

Contact us today to schedule a presentation and learn more—your success is our priority.

ABOUT

Flemington, NJ

QUICK LINKS

©2026 Preceptis Capital.

All Rights Reserved.

No Offer of Securities—Disclosure of Interests

Under no circumstances should any material at this site be used or considered as an offer to sell or a solicitation of any offer to buy an interest in any investment. Any such offer or solicitation will be made only by means of the Confidential Private Offering Memorandum relating to the particular investment. Access to information about the investments are limited to investors who either qualify as accredited investors within the meaning of the Securities Act of 1933, as amended, or those investors who generally are sophisticated in financial matters, such that they are capable of evaluating the merits and risks of prospective investments.